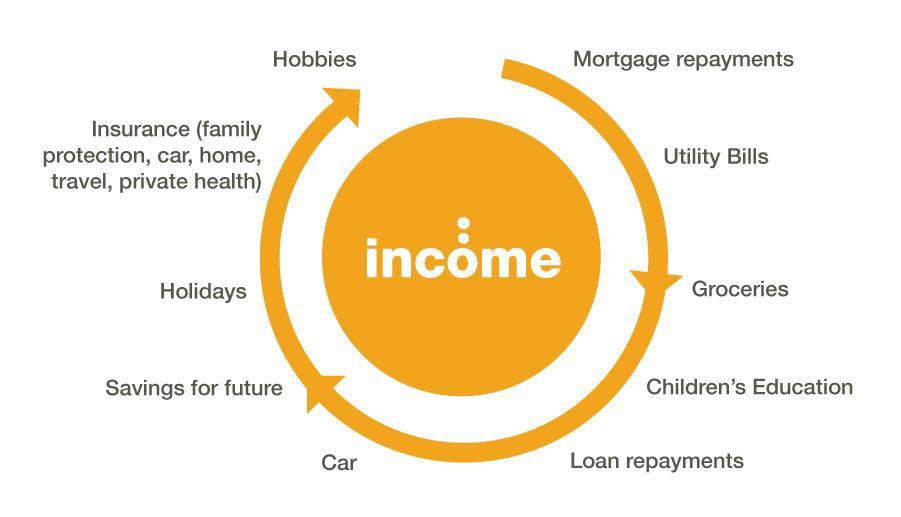

The concept of insurance has been there since the time civilization began to take its root, but income protection insurance is rather a modern notion. The policy is solely meant for the earning members of the society. It is true that most policies, which are sold in the market, are life insurance policies, but in this modern age one needs something more than that and income protection scheme is one of them.

What is Income Protection Insurance –

The words income protection tells a lot regarding the policy. It offers the policyholder protection, just in case there has been a loss of income due to sickness or accident related issues. However, here is a word of caution for the policyholder. This is not an alternative to unemployment. The policy is certainly not a cover for lost jobs due to dismissal or criminal actions.

http://www.youtube.com/watch?v=PRnnlIAwF18

From Where To Buy Income Protection Cover –

Now the next focus is from where to buy income protection Preexisting Medical Conditions cover. There are plenty of insurance companies selling the policy and with most of them having online presence, locating someone should hardly be a worry. The quotes or to be precise lower premiums are certainly a criterion. Nevertheless, the record of a particular firm in regards to claims payments should certainly receive focus. After all, the whole issue of buying protection is to receive benefits just in case there is a financial crisis. The amount of benefit too should get proper attention.

Why The Payout Is Limited To 70% Of The Last Income Drawn –

In general, the idea is to encourage the patient to get back to work. However, if the monetary payment exceeds the client’s income, then few will want to go back to work. Hence, on most instances, insurance companies try to curb the payout limit to 70% of the income. One can always do a comparative study of the offers and then choose accordingly. To get a better deal, one can even consult insurance brokers. They are not attached to any insurance company. Hence, they will certainly offer the best.

What Is Deferred Period –

The deferred period is another area to focus on. It is the period in between a claim and commencement of benefits. The longer is the period; the lower is the premium to be paid. However long deferred period may create trouble for those with limited saving and hence one should ponder over such points before picking up a income protection insurance.